Gravity (GRVY), the Sleeper, gets its pre-Q3 earnings updates

Ahead of Q3 release, let's look at why were Q2 earnings so disappointing, and how their mobile games performed in Q3.

We estimate mobile revenue based on Apple and Google App grossing ranks.

Gravity (Nasdaq:GRVY) will release their Q3 earnings on Nov 12 before the open. We have been covering GRVY (Datasheet) again since October 2022 in our initiation article, when we loaded the truck at $46.2 following a certain Origin release in Taiwan that was ignored by investors.

Previous Gravity updates/articles:

Executive Summary

Gravity announced much lower revenue ($93M) and net profit ($9.5M) than we expected for Q2, due to what seems to be a poor deal with Ruyi, the publisher of Ragnarok Origin in China

Investors have reacted rather vigorously to the earnings and knocked the stock off his 52W high of $88 in June to sub $60s. It’s now at $65.

Q3 is looking stronger than Q2 and it’s likely that 2024 will end up being an even better year than 2022. Can’t beat 2023, though.

Our thesis our Gravity is a story of drastic undervaluation and strong core business, and it remains intact with a PE < 7

Here’s 2024-H1 vs past 8 years of business

Q2 surprise explained

In spite of strong releases, such as Origin in China (March 27th, so a full quarter), Battle of the Novice Hearts, now called The Ragnarok (June 5th, only 1 month in Q2), revenue was flat QoQ and most of all, net profits dwindled. Why is that?

That really took us by surprise, since:

Origin Brazil doing really well

Origin China decent release. China is a humongous market in terms of mobile app spending, and even if didn’t stick for very long up there, Origin was in the top 20-30 grossing at launch.

The Ragnarok’s success in Taiwan seemed like a golden cherry on top of an already well iced cake

So what happened ? Yet, if you read their press release, there is absolutely no mention of Ragnarok Origin in China. That’s quite uncanny, given:

It was a major milestone for Gravity, to release a new game in China on mobile. It had not happened in years.

Their usual quarterly reporting is basically a barely digestible and pretty long list of games that increased and decreased in revenue and profit QoQ.

The game was released at the very end of Q1, and therefore had a full run in Q2. It was in the top 20-30 grossing on app store ranks at launch, which is quite good.

How is it possible that RO China was not even mentioned as a revenue driver? We contacted IR and their explanation is that “Origin did not do as well as expected in China”. However, apple store ranks do not lie. The game has done fairly well (cf previous post) in China.

We tried getting more information on the shape of the deal with Ruyi, the game publisher in China, but they of course refuse to share anything about the agreement.

However, Ruyi released their own H1 results, and this is what they had to say about Ragnarok Origin in their report:

They certainly sounded more optimistic, with a first month exceeding $14M of “cash flow”.

The likeliest scenario is that they made a pretty poor deal with Ruyi. Speculations only here:

They could have agreed to a very low royalty %.

There could be a minimum threshold of revenue the game needs to achieve, after which only they start receiving royalties. That threshold may have been too high to even hit in Q2.

The more optimists in the room may argue that “maybe they just did not factor in Origin in Q2 due to [insert an accounting reason here].” Given the strict rules Gravity has to adhere too by being traded on the Nasdaq, and the fact IR said that the game disappointed, it’s probably safer to be conservative and discard this eventuality.

Looking ahead - the operations

Lots of actions end of Q2 and in Q3

Some updates about Q3 results and the games that moved the needle.

Here's a breakdown per month and per game of estimated revenue for each mobile game (keep in mind it’s based on app grossing ranks, not real revenue)

End of Q2, 3 new games were released:

June 6th: The Ragnarok (Novice Hearts) in Taiwan and Hong Kong

The game was well received and stayed in the top 10-15 grossing (all apps) in Taiwan for 4 months. It’s now in the top 20-30 daily. Taiwan is a major market as we keep repeating. If you recall, Origin’s success in Taiwan (stayed in the top 5 for months and months) was the reason we invested in Gravity again in October 2022.June 27th: Rebirth in SEA (TH, PH, ID, SG, MY)

Brand new game released in SEA. It got to a soft start as a top 20 in most countries. After 5 months it’s in the top 150-200. Clearly not as strong a contender as The Ragnarok, which is bound to hit SEA this year.June 28th: Ragnarok Online on PC in (Launched June 28th) in China.

Hard to measure success given it’s a PC game and in China, but it was highly ranked on “WeGame”, a local Steam competitor, for a few weeks at launch. We’ll be looking at the % of revenue from PC vs mobile in Q3 to gage its real success.

In Q3:

Sept 13th: Next-Generation was released in China.

Total flop, unfortunately. Butchered launch, I would expect the publisher to press reset on this.Sept 21st: The Ragnarok was released in South Korea.

Fairly disappointing, the game hit the top 20-30 at launched but fairly quickly fizzled out to the top 50 after a month of live operations. It seems’ Ragnarok franchise power in Korea is not as strong as in SEA and Taiwan/HK.

Overall, based on mobile ranks, we estimate that The Ragnarok could be driving about 45% of Gravity’s mobile revenue in Q3, with Origin (World) still pulling its weight as the 2nd game (but definitely getting lower Q on Q).

Eternal Love and Next-Gen still delivering that long tail revenue and profitability!

Q3 poised to be stronger than Q2 (ignoring China)

Extracting from ranks data, we think mobile revenue in Q3 will beat those of Q2 by approx. 15%. That’s all ballpark obviously.

Then there’s non-mobile revenue, where the big question mark is Ragnarok Online PC in China. We’ll assume no major revenue there.

In terms of profitability, it’s likely most of the marketing cost for The Ragnarok was carried in Q2, so we hope to see the net profit margin go back to the 15%-20% range we’ve been used to before Q2-2024.

Our guesstimate for Q3 is:

$100-110 millions in revenue

$15-20 millions in net profits

This would make Q3 stronger than both Q1 and Q2.

Closing 2024 and going into 2025

Gravity still have a few tricks up their sleeves for 2024. We are quite excited to see The Ragnarok going to SEA in Q4. Origin drove major revenue over there after all, and it seems to be the logical ‘successor’ based on its reception in Taiwan and South Korea.

Other interesting releases likely planned for 2024 in our opinion include:

RO: Next Gen in Japan. It’s a proven game, and Japan is the 3rd largest mobile market in the world.

Ragnarok in Wonderland (new game) in Korea

NBA Rise (Reboot, they failed the first launch) in Japan.

With that, in all likelihood, FY2024 will finish slightly upwards of FY2022 but short of the exceptional FY2023. The stock has been punished quite a bit for that already.

Going into 2025, it appears Gravity will be rolling out many game, and that they will also be targeting a new market for their mobile games: Europe, by rolling out 2 of their most successful games: Ragnarok Origin and Next-Generation.

They also keep on throwing spaghettis at the wall by publishing indie studio games on PC/Console and mobile - who knows whether one will stick. We don’t.

Valuation, and an activist investor at Gungho

Strategic Capital enters the chat

In October, an investor fund by the name of Strategic Capital, which has in the past been portrayed as an activist investor, became Gungho’s 2nd bigger shareholder by snatching about 5.5% of their shares. Activist investors are named as such because they generally try to take an active part in generating shareholder value.

As a reminder, GungHo is the Japanese company that owns over 59% of Gravity shares, meaning that Gravity is a non wholly-owned subsidiary of GungHo.

Now, it’s anyone’s guess what Strategic Capital sees in GungHo, but one thing is certain, they are buying because they believe they can increase GungHo share value significantly.

Following the announcement of Strategic Capital taking a position, both GungHo and Gravity shares rose spectacularly, with GRVY gaining 15% in 2 days. Based on volume and timing, it does not seem they themselves acquired those shares in GRVY, and the hike in price was likely due to investor reacting to the news.

Make that what you will, we will not speculate. Gravity’s investors are probably hoping Strategic Capital will do something about the cash hoarding of the subsidiary:

We see positively an activist embarking the mothership, and we hope that whatever plan they have, also brings value for Gravity shareholders.

Valuation of GRVY as of October

Our initial case for Gravity from October 2022 rested on 2 facts:

Ragnarok Origin’s massive success in Taiwan and Hong Kong was ignored by the market

Gravity’s valuation was far below its peers

2 years in - Gravity rose 40% to today’s value of $65. That all sounds good until you realize that’s a -33% alpha against the NASDAQ, which is.. staggering.

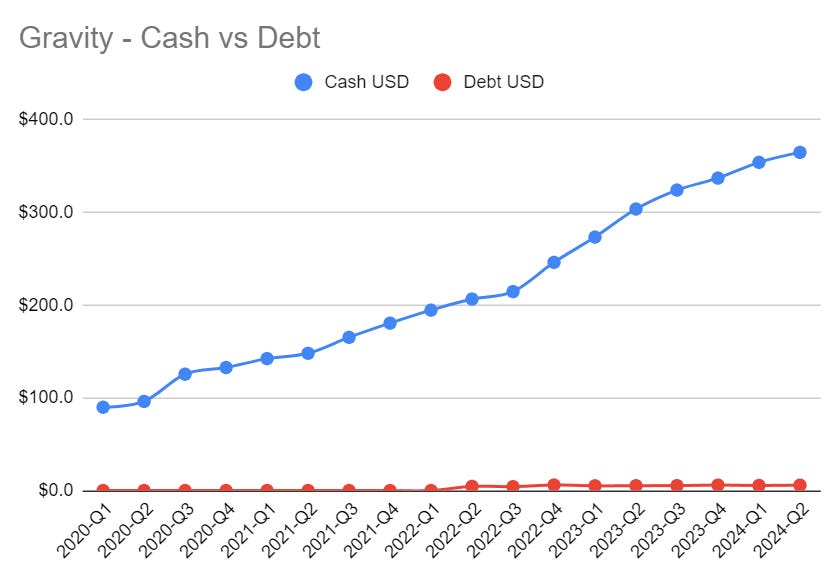

So, how’s GRVY valuation looking at $65? With about $365M in cash vs $5.8M in debt (Q2), market capitalization stands at $450M and enterprise value at a meager $94M, the lowest since we bought in Q4-2022!

That’s for a company with:

FY2024 revenue to be around $400M, with a net profit margin in the 15%-20% range, after 8 years of growth on revenue and profitability

TTM PE of 6.9, and that’s with last quarter’s profitability being abnormally low due to major marketing expenses.. EV is at about 1.5x EBIT.

TTM EV/Sales of 0.2. Talk about a discount.

Our opinion is that Gravity remains extremely cheap, and would still be below most of their peers valuations if the stock doubled from current value!

You will therefore not be surprised to hear that we bought some more shares at $57-$60 this quarter.

Conclusion

Origin China disappointed on revenue, and Next-Gen launched was inexistant. Yet the company is still set to grow 2024 vs 2022. 2023 will remain an anomaly for now.

Gravity remains our favorite risk/reward on the basis of their low PE, strong earnings and growth prospects. You are currently paying less than 1.5x EBIT for the stock.

The arrival of an activist investor at GungHo, a strong balance sheet against the backdrop of an industry filled with bankruptcy and layoffs in the past year, it looks like the tree could be about to be shaken up a bit. We’re hoping for smart acquisitions, and dividends. That’s on our Christmas list.

Disclaimer

The information on this website and blog is for educational and informational purposes only and should not be construed as professional investment advice. Please consult with a licensed financial advisor before making any investment decisions based on the information provided on this website. We do not endorse any particular investment product or strategy, and you should make your own decisions based on your own research, risk tolerance, and financial circumstances.

while I found you because of Gravity, I would like to ask you what is the real market reach and market share of Yalla