This Tiny App Maker Just Tripled in 60 Days

How we tracked grossing ranks to spot profitability before the market did

A reminder about our App Investing concept.

Our core idea is simple: iOS/Android app store grossing ranks are forward-looking financials. When a small publisher’s game start climbing, we can back-out daily revenue and map it to the listed parent. That’s where our “value-meets-swing” approach lives: patient tracking until a catalyst appears.

Intro to Feiyu Technology (1022.HK)

Feiyu is a Xiamen-based (China) studio founded by a Fujian team in 2009, originally building web RPGs and then moving into mobile (first mobile launch in January 2012).

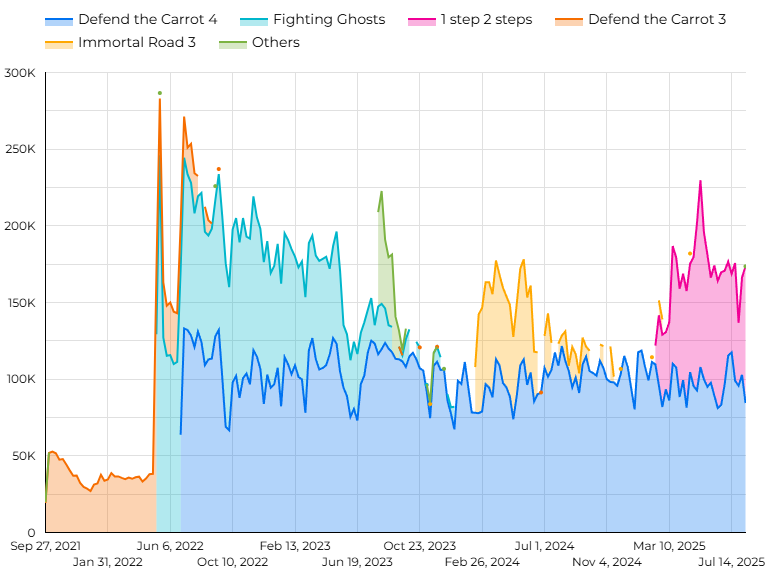

Pre-IPO, Feiyu’s portfolio mixed long-running web titles like Shen Xian Dao (2011 web; 2012 mobile) and Da Hua Shen Xian with casual mobile successes; in late 2013 it acquired the Carrot Fantasy (保卫萝卜) franchise, which ranked among China’s top casual games by users and time spent in 2013–H1’14, per its prospectus.

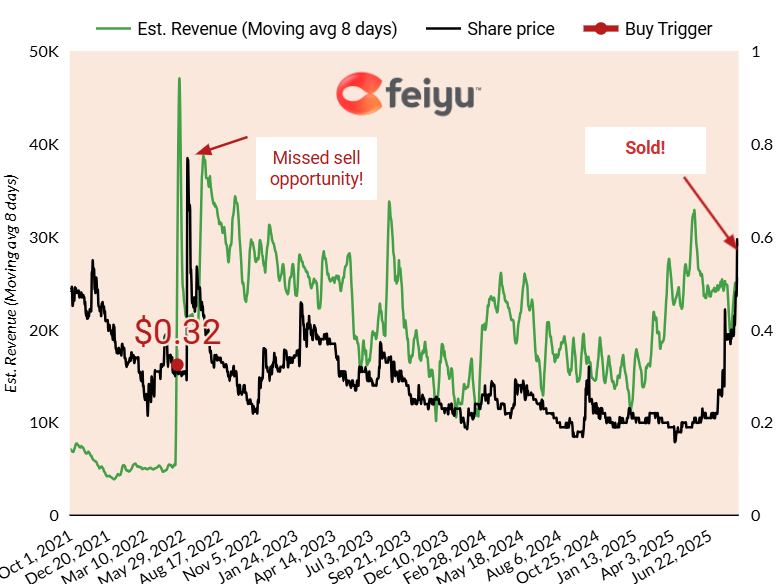

Feiyu listed in Hong Kong on December 5, 2014 at HK$2.20 per share, raising roughly US$85m to fund new games, marketing, overseas expansion and M&A. By the moment we purchased to stock in 2022, it was in the HK$0.30s

The Feiyu thesis (and why we were comfortable holding it)

We first highlighted Feiyu in our initial article in May 2022 when “Fighting Ghosts” (or “Fight Tricks”) spiked revenue; and after a massive stock hike which we definitely should’ve sold (cf chart below), for much of 2023–24 the market yawned.

Stock reacted promptly but we missed the sell opportunity. However it was clear revenue was above previous baseline.

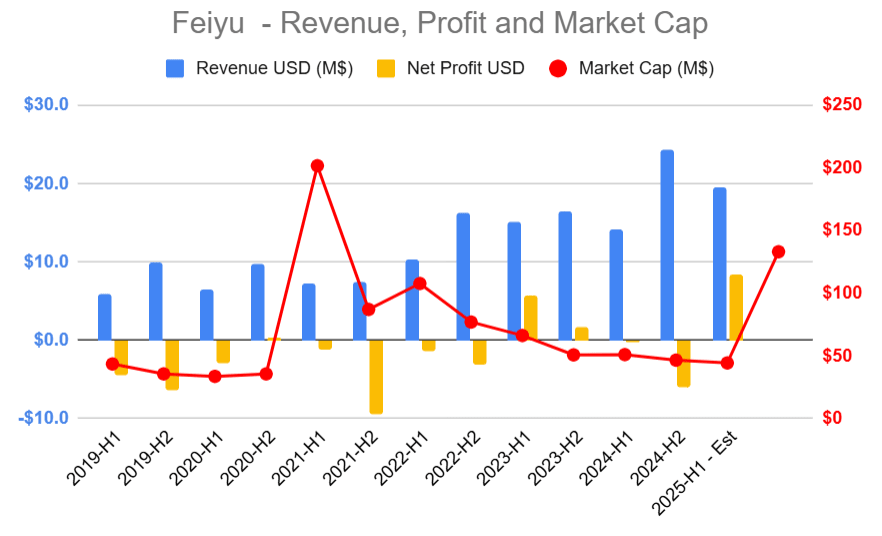

We kept watching the charts and the financial footing. By FY-2023, Feiyu swung to a RMB 52.2 m profit after a 2022 loss and ended the year with RMB 160.7 m in cash and equivalents; interest-bearing bank loans stood around RMB 95.5 m, a modest leverage level for a studio running low-cost live-ops. That balance-sheet cushion made us comfortable staying the course while the market ignored the improving P&L and cash profile.

Whilst the market ignored it, we stayed the course and we purchased more shares in early 2024, presenting the updated thesis in this article: Feiyu is doing well, its stock isn’t. We why averaged down.

Another catalyst: 1 Step 2 Steps

Early 2025, casual title 1 Step 2 Steps lifted Feiyu’s baseline revenue without big UA bills. Classic Feiyu: sticky live-ops, low marketing. Nobody reacted. We could have added more, but given the low liquidity of that stock, we did not take the risk. A shame, because at that point the stock was trading in the low HK$0.20s, a third of today’s price. And that’s just a few months back.

Estimated weekly revenue per game for Feiyu. Only considers iOS revenue - we generally use a rule of thumb of Android revenue = 2x iOS revenue in China.

Profit alert and re-rating

On July 23, 2025, management issued a positive profit alert guiding RMB 55–70 m net profit for H1 2025 (vs. a small loss in H1 2024). The stock promptly re-rated, roughly tripling from ~HK$0.20 in June to HK$0.60 by mid-August (note: HK$0.60, not HK$60).

Trade and outcome: take the win

We sold our shares of 1022.HK this week at HK$0.60. We first bought at HK$0.32 (May 2022), averaged down at HK$0.25 (September 2024), for an average entry of HK$0.285. That’s a ~110% ROI at exit. For fairness, we compare to the NASDAQ Composite which was sitting at lows, and went from 11,747 to 21,210 in the meantime, a +80% ROI, giving us a solid +30% αlpha.

Could Feiyu run further? Sure. But after a clean catalyst, profitable H1, and a 3x move in two months, we’d rather book the gain and scan for the next setup. One where the stock has more liquidity and interest, so we don’t have to wait 3 years to book our gains.

Why subscribe?

This is the playbook: track grossing ranks, translate them into revenue, and pounce when the market is asleep. Feiyu went from overlooked to obvious, and fast. Follow us to stay current on the mobile market and the next swing-trading opportunities that look just like this one, as well as weekly mobile app revenue trends.